After having my 30th birthday last month, I thought it was time to reflect on the past decade, especially the key money lessons I learned in my 20s.

Your 20s are a time of self-exploration and learning adulting — including making money and learning to manage your own finances. As far as I can remember, I’ve always been lucky to have a healthy relationship with money and been good at living within my means. This has helped me to avoid any major, reckless money mistakes. However, there are still things I wish I’d known earlier or perhaps done differently!

To save you from learning the hard way — and pass on some knowledge — here are the top five money lessons I learned in my 20s.

Invest, invest & invest

If I could give myself in my early 20s one single piece of money advice, it would be to start investing as soon as possible. Saving is great but simply not enough. For most of my early 20s, I kept saving money without really knowing what I’m saving it for.

The reason why I didn’t start investing in stocks earlier was that I always assumed it would be complicated and that I would need a lot of money to do that. It wasn’t until I was 29 that I educated myself more on the topic and understood that neither of my assumptions was true. In fact, things such as Stocks & Shares ISA and index funds/ETFs make it pretty simple.

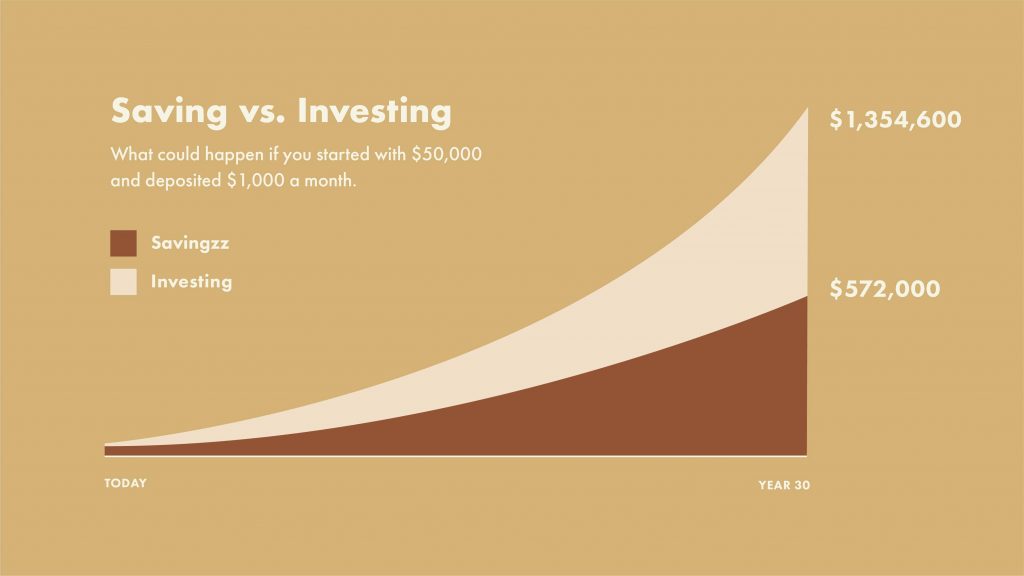

So why is investing so important? The key reason to start investing early lies in the power of compound interest – “the eighth wonder of the world”. The earlier you start, the longer your money has time to grow and compound.

Still not convinced? Have a look at the below graphs that show the difference between saving vs investing and the difference starting 10 years later can make.

Set financial goals

The next money lesson I learned in my 20s is the importance of setting financial goals. Goals will help to give you direction when it comes to money. Remember that your money habits today will impact your financial security in the future.

It’s easy to dismiss this in your early 20s because it feels like you have all the time in the world before having to worry about things like buying your first home, saving for a wedding or financially preparing for having a baby. But trust me, it’s better to prepare for these types of financial commitments in advance.

Even if your goals are more short-term and fun-focused (like buying a luxury investment handbag or saving for your dream holiday), it still helps to set a specific amount you want to save by a certain time. To help you to keep your eyes on the prize, it can be very motivating to visualise what you are saving for and why.

When deciding on your financial goals, try to set SMART goals. SMART stands for Specific, Measurable, Achievable, Relevant, and Time-Bound. In other words, be as specific and detailed as possible with your goals.

Related: How to Set Savings Goals

Invest in yourself

Your twenties are a great time to enhance your skills and knowledge levels, including personal finance education. Improving your skills doesn’t always mean investing in higher education or even formal education, although that’s surely one option (and potentially a necessary one depending on your career field). However, investing in your knowledge and skills can take many forms.

Apart from my university degrees, I invested in things such as a business and property course and online digital marketing qualification in my 20s. All of these have helped in my career and my investing journey. However, investing in yourself doesn’t always even need to cost money. In fact, I’ve gained most of my property investing knowledge by watching hours and hours of YouTube videos and by attending property investors’ networking events.

While investing in your skills and knowledge is essential, it’s also important to invest in your physical and mental wellbeing and happiness. For me, this means things such as exercising regularly, meditating and spending money on experiences like travelling.

Build multiple streams of income

One of the most important money lessons I learned in my 20s is the importance of multiple income streams. In my early twenties, I used to think that salary from a full-time job is all I need to live a comfortable life (funnily enough, I didn’t even earn much at that time). When I was made redundant from my first ‘proper job’ and later learned about the principles of financial freedom, it became crystal clear why having multiple streams of income is important.

In addition to greater financial stability and security, having multiple income streams can help you reach your financial goals faster. If you work a 9-5 job, one way of maximising your income is by taking on a side hustle or creating passive income streams (if you already have some money to invest). My first additional income came from subleasing a spare room in an apartment I lived in (with the landlord’s permission of course). Later on, when I purchased my first home in my mid-20s, I continued renting out my spare room, this time for short-term guests through Airbnb. (Did you know there are actually plenty of ways to make money from Airbnb without owning a property?)

Don't compare yourself to others

Personal finance is called PERSONAL for a reason. Therefore, when it comes to money and success, comparing yourself to others won’t take you far. While it’s fine to have other people as role models or sources of inspiration, comparing yourself to them isn’t a good idea.

Many times, this comparison just leads to not-so-smart money decisions like spending recklessly or getting into debt in order to keep up with the Joneses. Even if you managed to keep your finances in order, comparing your salary or job title to someone else’s is likely just going to cause you unnecessary stress. Furthermore, neither of these is a good measure of one’s success or happiness.

While this is something I’ve learned in my 20s, I can’t say I’ve fully mastered it yet. But rather than comparing, it’s important for us to lay our focus on setting our own financial goals and following them. To do this, you will have to plan your own way and patiently follow it.

Again, personal finance is personal to each individual. Even this list of money lessons would look completely different written by someone with a different background, life path and goals.

What’s the most important money lesson you have learned in your life?

I wish I had learned these same lessons in my 20’s. I am glad you had a family who taught you the value of healthy money management, coming from such a family really does make a world of difference.

Thanks for your comment, Nadia. Although everything I listed here is self-thought (many of these are things my family don’t do), I can’t deny the impact that my family and personal circumstances must have had on what I learned while growing up, helping me to build a strong base to learn more. However, the good news is that it’s never too late to start educating yourself about personal finance and improving your money situation, no matter your past and current circumstances 🙂

I started investing a few years ago and I wish I would’ve learned about it at a younger age. But better late than never. I enjoyed reading your blog post.

Glad you enjoyed the post and thanks for sharing your experience too! 🙂

These are great lessons! I think my top advice for anyone is to start early. Even if it is just saving 100 a month in a retirement plan when you are in your early 20’s. That money will have so long to grow, you will end up with 4 or 5 times that amount when you are ready to retire. Great suggestions!

I 100% agree! Whether it was saving or investing, starting early is key and can make a huge difference in the long run.

Absolutely! Invest in yourself and don’t compare! Thank you for sharing.

These are great tips! I’m in my early 20s and I’m this year my goal is to stick to a budget.